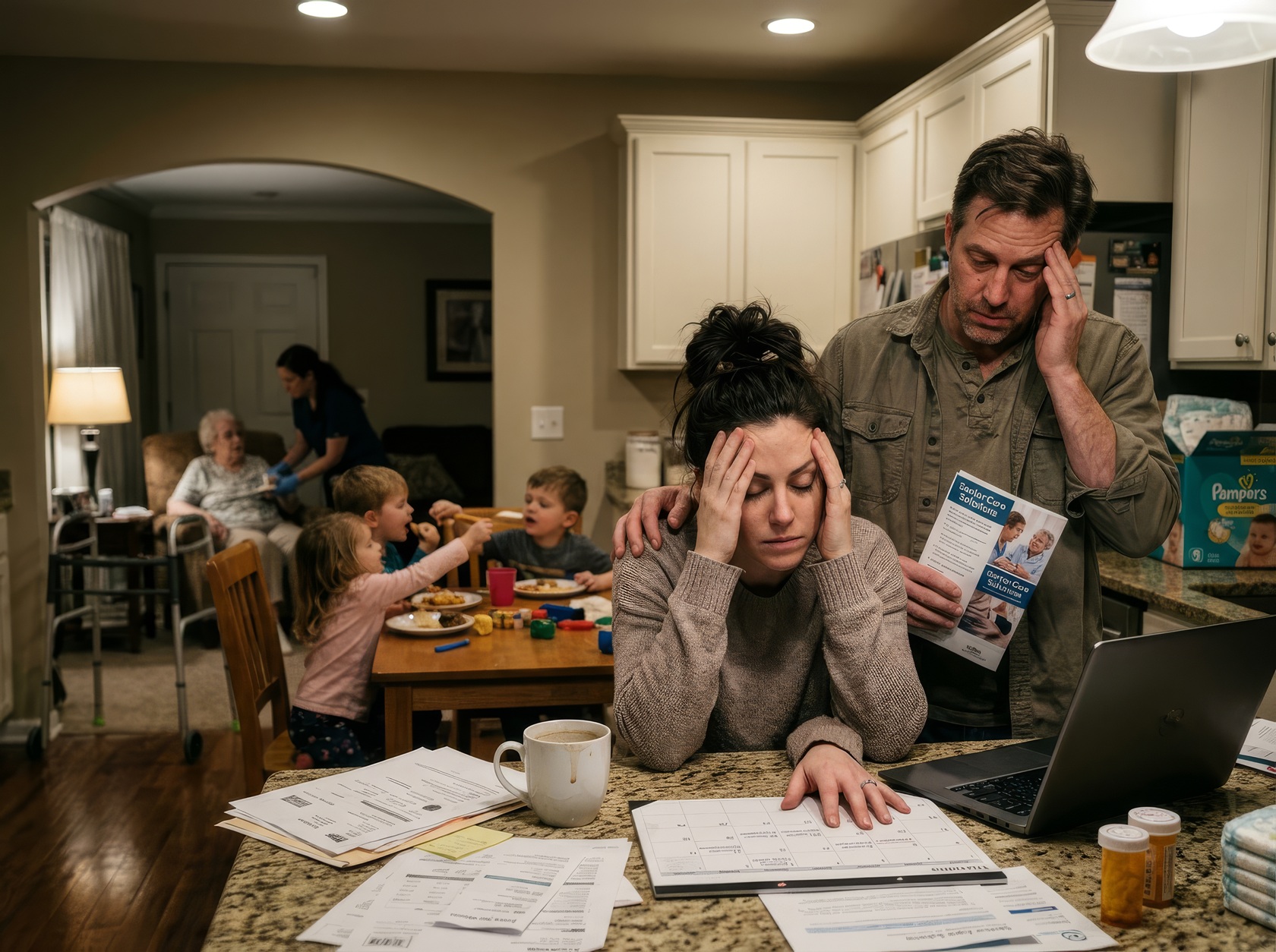

Members of the so-called “sandwich generation” often feel trapped by unique pressures. They must balance the escalating costs of raising children while simultaneously managing the care of aging parents.

Today’s 40- and 50-year-olds frequently find themselves with parents in their 80s and children in their teens or younger. Managing these dual roles can introduce incredible stress and effort into daily family life.

A few years ago, we discovered an insightful article from the financial site NerdWallet in which writer Kate Ashford addresses the challenges of caring for aging parents and growing kids. We are sharing these key tips once again to provide encouragement and clarity as you manage these competing family demands.

The Financial and Emotional Strain of Dual Caregiving

Ashford begins her article with some startling stats: “Nearly a quarter of millennials are caregivers for an adult, according to a 2020 AARP survey. And a 2020 report from insurance marketplace GoHealth found that 1 in 3 millennials are supporting their parents financially, and more than a quarter help manage their parents’ health care.”

In practical terms, this means that many millennials are caring for young children as well as caring for aging parents, grandparents, or other aging loved ones. “That can take a toll,” Ashford writes. “Eighty-two percent of millennials worry about having enough money to support both their parents and themselves, according to GoHealth.”

If you are currently feeling squeezed by these modern family dynamics, you can access specific resources to lessen the burden. Ashford highlights several strategic avenues to help manage these rising caregiving costs.

One Starting Place: Long-Term Care Insurance and Home Equity

If you’re dealing with the costs of caregiving for a parent, the first place to look for assistance will be to see if they have any form of long-term care insurance. This coverage can help with either in-home care costs or assisted living and/or nursing home expenses.

“I’ve talked to a lot of caregivers who didn’t even know their loved ones had long-term care policies,” says Amy Goyer, AARP’s caregiving expert. “That can be very, very helpful.”

A reverse mortgage is also a possibility, if the person you’re caring for has enough equity in their home and they’re 62 or older. “A reverse mortgage provides a loan or line of credit based on equity in a home. But it’s not right for everyone,” Ashford writes.

“I always recommend talking to a financial advisor, especially someone who has a lot of experience with reverse mortgages, before you get into one,” Goyer says.

You May Qualify for Caregiver Tax Credits and Deductions

Federal tax credits and deductions are often available for those who can claim their aging parent or loved one as a dependent, meaning they’ve provided over half of their financial support for the year.

“The child and dependent care tax credit can apply to seniors,” says Jill McNamara, senior director of online care marketplace Care.com. “This opens the opportunity for caregivers to save annually on their expenses related to in-home care or adult day care services.

Additionally, there is the credit for other dependents, which allows caregivers access to a $500 credit.”

This can extend to medical expenses, too. Ashford explains, “If you’re paying your loved one’s medical expenses, you’re also eligible to deduct medical costs that exceed 7.5 percent of your adjusted gross income. This includes health care, prescription drugs and transportation for medical care, among other things. (See IRS Publication 502 for a full list.)”

Veterans Benefits and Government Programs Help Those Who Qualify

Is your loved one a veteran? It’s worth checking to see if they are eligible for benefits through the Department of Veterans Affairs (check caregiver.va.gov). These benefits may include access to health care, medical equipment, and even home modifications.

“My dad was able to get all of his medications without a copay,” says Goyer. She also received help setting up hospice care for her father and getting a household ramp installed. “Never assume they won’t qualify. Keep asking the questions and find out. We got incontinence supplies, which is a huge expense,” she adds.

Navigating Medicaid: Get the Right Advice from an Expert

If your loved one has a low income, Medicaid can help. But do your research; every state’s rules are different. We suggest families meet with an objective professional who knows the ropes when it comes to Medicaid.

“A note of caution: If you’re caring for a parent, don’t combine your money with your parent’s money,” Ashford warns. That’s because doing so can disqualify your parent from benefits.

“If a parent is ever going to need Medicaid, Medicaid has a lookback period,” says Pamela Wilson, a caregiving expert and speaker. “They don’t like combined accounts.”

Ashford continues, “A person needs to have a very low income and/or limited resources to qualify for Medicaid. If levels aren’t low enough, you may be able to plan a strategic spend-down of assets. Goyer recommends talking to a certified Medicaid planner (you can find one at cmpboard.org) or an eldercare attorney for advice.”

Contact us and we’d be glad to assist you in your planning.

Don’t Overlook Community Agencies and Support Networks

Thinking local can apply to caregiving, too. State or city programs local to your loved one could help with prescription drug costs, doctors’ bills, groceries, and other expenses.

“AARP offers links to state-by-state benefits available, and you can also check with your area agency on aging,” Ashford writes. “Caregiving advocacy organizations can be helpful. The Caregiver Action Network offers free advice by phone, email or chat at caregiveraction.org.”

The Caregiver Action Network’s CEO, Marvell Adams Jr., says, “Someone could call our help desk and say, ‘I just realized my mom’s copays for her prescription drugs have really eaten up a lot of her savings and she’s having difficulty paying them.’ And we say, ‘We can connect you with a copay assistance foundation.’”

Also of note, The National Council on Aging offers a Benefits CheckUp tool to screen for eligibility for hundreds of programs that can help with costs.

Protect Your Financial Future with Professional Planning

Consulting with a financial planner is always a good first step to make sure you’re making the right decisions for your unique situation – and for the health of your financial future, too. “As a caregiver, we start paying for things and we get ourselves into a difficult situation,” Goyer says.

Ashford advises using two different planners. “I think it’s helpful to have someone who’s really looking at your picture,” Goyer says, concluding the article. “And help[ing] you make hard decisions that will, in the long run, protect you as a caregiver.”

Rajiv Nagaich: Your Retirement Planning Coach and Guide

Rajiv Nagaich’s newest program on PBS, called Designing Your Ideal Future, is bringing Rajiv’s powerful message to Americans from coast to coast. This engaging and challenging PBS show is prompting thousands to take a fresh look at the type of planning that will help them succeed in retirement.

In this one-hour PBS special, Rajiv Nagaich takes viewers step-by-step through the principles of creating a retirement plan that truly supports the life you want to live. Instead of generic check-the-box paperwork, Rajiv reveals how to infuse your perspective — your values, goals, and priorities — into every legal document and life plan component so your plan becomes a living system for your future.

Designing Your Ideal Future includes insights from real-world planning examples and a live Q&A with Rajiv Nagaich that answers viewer questions about retirement planning, legal readiness, and family communication. It’s perfect for anyone approaching retirement, currently retired, or responsible for a loved one’s future care — and for those who want a clear, effective approach to planning that prioritizes personal choice and quality of life.

What About Your Own Retirement Strategy?

You’ve heard Rajiv say it repeatedly: 70 percent of retirement plans will fail. If you know someone whose retirement turned into a nightmare when they were forced into a nursing home, went broke paying for care, or became a burden to their families – and you want to make sure it doesn’t happen to you – then these materials are your key to retirement success.

Visit your local PBS station’s schedule to find airtimes and learn how to access companion resources — including a free Legal Readiness Quiz and tools to help build your complete LifePlanning system.

Don’t remain among the millions of Americans sleepwalking their way into a retirement they never wanted. Instead, your retirement can be the exciting and fulfilling life you’ve always hoped it would be. Start by watching, reading and sharing Rajiv’s important message.

And remember, Age On, everyone!

The post Caught in the Sandwich: Caring for Aging Parents, Raising Your Own Kids appeared first on Home.